Gold rose 6X over the past 20 years.

Over that period Newmont is up only 16%, basically unchanged.

Most of the majors are currently trading at the same price they were 20 years ago.

Let me tell you why.

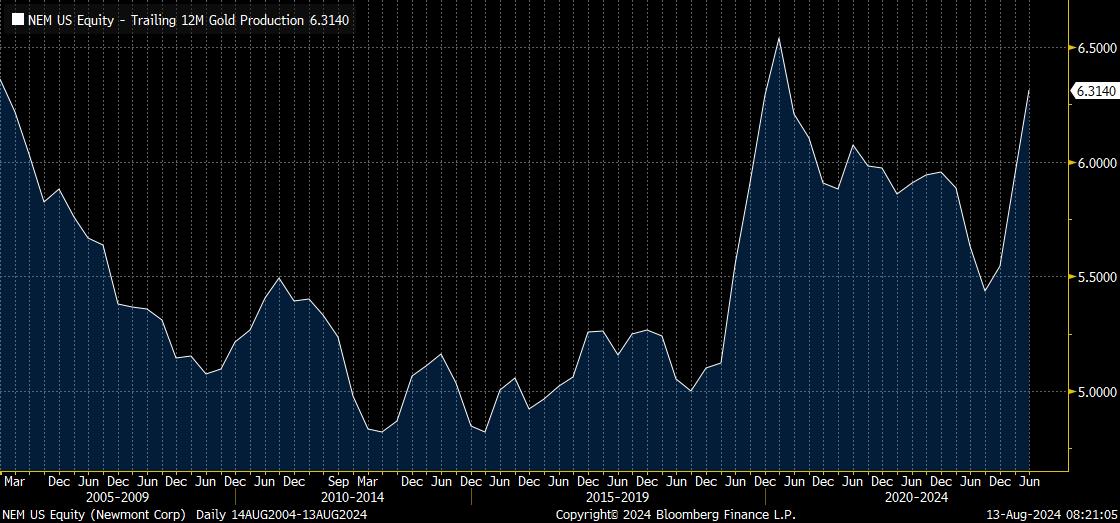

First of all, Newmont’s production is at about 6.3 mil gold oz per year.

The same as it was 20 years ago.

You would assume Newmont is making more profits with gold at $2,500/oz.

Over the past two decades Gold rose 6X from $420/oz to $2,469/oz.

But look how Newmont’s cash costs rose 5X from $239/oz to $1,152/oz over twenty years.

Newmont’s gross margins are at 47%. The same as 20 years ago.

While true that 47% margin is worth $1,160/oz now vs only $197/oz in 2004, gross margins haven’t changed over 20 years.

Productivity and technological enhancements are minimal.

Mining and processing is basically done the same way as 100 years ago.

The increased profits per ounce, are entirely due to the rise in the gold price.

Take a look at Newmont’s gross profits.

6X growth from $413 mil to $2,246 mil over the past 20 years.

Since stock price track profits you would assume Newmont stock would have climbed 6X as well.

But it didn’t. Newmont’s stock has barely moved in 20 years.

Look at Newmont’ market cap rising from $20 bil in 2004 to $56 bil now.

Surely the stock must have done great…Nope.

An increase in market cap doesn’t mean shareholders made out well.

Bankers and management get paid more when the market cap rises.

But shareholders get screwed.

Because Newmont’s shares outstanding rose 3X from 400 mil in 2004 to 1,152 mil now causing economics to decline on a per share basis.

Newmont currently makes $1.95 in gross profits per share.

While higher than $1.00 per share in 2004.

Gross profits are the same as they were in 2007.

And much lower than peak $3.50 per share when the GDX and Newmont’s stock price topped out in 2011.

Mining is a tough business, and the stock prices reflect that.

There is a better way to capitalize upon rising gold prices.

That’s why I started the Golden Portfolio (GP).

Focused on a sector of the gold mining space whose costs never change.

With the ability to turn $100K into 100K gold ounces.

Turning $100K into $250 mil of shareholder value at todays gold price

And leveraged to the gold price and exploration success at no additional expense.

The GP is already up 19% YTD, and gold is just beginning to break out.

I also created the GP10X.

Grade and people focused.

Because grade drive profits, and profits drive stocks.

A single high-grade drill hole can create hundreds of millions of shareholder value overnight.

Aligned with management dedicated to increasing economics on a per share basis.

The GP10X has 5 holdings already up over 100% YTD.

The GP10X are already up 26% YTD.

Click here to receive my free e-letter direct to your inbox for more insights like these.